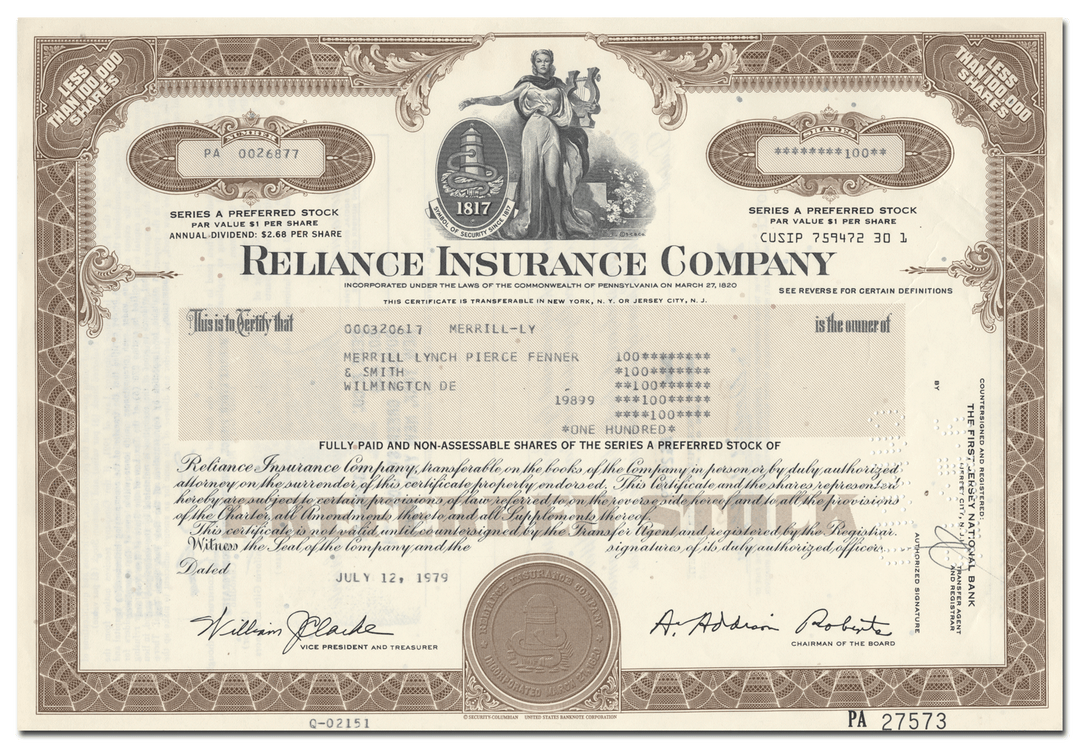

Reliance Insurance Company

- Only 4 left!!

- Backordered, shipping soon

- Guaranteed authentic document

- Orders over $200 ship FREE to U. S. addresses

Product Details

CompanyReliance Insurance Company

Certificate Type

Series A Preferred Stock

Date Issued

1970's

Canceled

Yes

Printer

Security-Columbian/United States Bank Note Company

Signatures

Machine printed

Approximate Size

12" (w) by 8" (h)

Images

Representative of the piece you will receive

Guaranteed Authentic

Yes

Additional Details

NA

Historical Context

Reliance was founded in 1817, officially incorporating in 1820, as the Fire Association of Philadelphia, organized by 5 hose and 11 engine fire companies. Upon inception, Reliance became the nation's first successful association of volunteer fire departments, which beforehand had been independent of one another and often engaged in inefficient competition, which at times extended to the destruction of rivals' equipment and the assault of rival firefighters. In addition to underwriting fire insurance, the association served as mediator between its member engine and hose companies to resolve the problems of the past. The association's first policy was bought by Samuel Bleight for his three-story building. One lasting symbol of the company adopted at the outset was the fire mark featuring a fireplug with a coiling hose and the initials F.A. on both sides.

The association was granted a charter by the governor of Pennsylvania on March 27, 1820, and wrote 29 policies that year. By 1832 the association wrote 583 policies and by 1844 it had 44 member companies. Eventually, it had a $100,000 surplus, all of which was lost by the Great Fire of Philadelphia that year. The trustees, however, paid all resulting claims, which brought them goodwill and led to further expansion. In 1871 the city of Philadelphia created its own fire department. In response, the trustees chose to continue as a stock company under a new charter, whereby they became solely an insurance company and began writing policies outside of Philadelphia.

The business continued to grow over the ensuing decades with the development of a countrywide field of agents, expanded forms of coverage including automobile insurance, and the formation of various subsidiaries, one of which was Reliance Insurance Company founded. Later, the association merged its subsidiaries into the parent company, and on January 1, 1958, The Fire Association of Philadelphia officially changed its name to Reliance Insurance Company. The company's growth continued through acquisition and the establishment of subsidiaries. The General Casualty Company of Wisconsin was bought in 1956 and United Pacific Insurance Company in May 1967, providing the company with a solid presence in the Midwest and West respectively. Eureka Insurance Company was started in 1959. Its name was changed to Planet Insurance Company in 1963, and beginning in 1976, wrote Reliance's commercial mass-marketing business.

In 1968 the brokerage firm of Carter, Berlind & Weill ("Carter Berlind") saw the potential in acquiring an insurance company, many of which had strong balance sheets and excess surplus, which could be used for other things outside of the insurance business. They examined several insurance companies and eventually targeted Reliance as the most attractive candidate because of its strong financial position and because a large percentage of the company's stock was owned by Carter Berlind's institutional clients thus making them prime for a takeover. After having approached and having been rejected by many other financiers, such as Laurence Tisch, Carter Berlind presented the idea of selling Reliance to Saul Phillip Steinberg.

Mr. Steinberg was born August 1939 in Brooklyn, NY, and received a Bachelor of Science degree in Economics from the Wharton School of Finance at the University of Pennsylvania in 1959. In 1961, at the age 22, he founded Leasco Data Processing Equipment Corporation, a small office data-processing equipment firm that leased IBM computers. The company grew rapidly, expanded its capabilities, and in 1965 went public. As Leasco grew, Steinberg sought to diversify the company. In 1968 Leasco bought 91% of Reliance Insurance Company and its subsidiaries (Steinberg bought the balance of the company in the winter of 1981). A year later in 1969 Steinberg attempted to take over the $9 billion Chemical Bank, then one of the nation's largest financial institutions. The attempt failed and earned Steinberg the enmity of the New York financial community and a reputation for brashness. Mr. Steinberg remarked at the time, "I always knew there was an establishment; I just thought I was part of it." Fifteen years later Steinberg would make another legendary run at another fabled American institution, The Walt Disney Co. He failed in this bid too, but forced Disney to pay him $60 million in "greenmail" for his shares.

Under the direction of Steinberg, Reliance and its corporate parent Leasco underwent significant changes in structure and operation. A holding company called Reliance Group Holdings was formed, which through an intermediate holding company owned Reliance and its subsidiaries and sister companies. In 1973 Leasco changed its name to Reliance Group, Inc., to reflect a corporate strategy away from computers services toward financial services and notably insurance-related ones. New insurance subsidiaries were spawned to handle the company's increasing expansion into selected specialty lines, including Commonwealth Land Title Insurance Company, Reliance Insurance Company of New York, Reliance Lloyds. Later, the expansion included the incorporation of several new life insurance companies. Throughout this period of expansion and diversification, Reliance Insurance Company continued to handle most of the standard lines of insurance with which most people are familiar, including personal automobile and homeowners.

In 1981 Steinberg, still chairman of the board and chief executive officer, acquired all outstanding shares of Reliance Group, Inc. Thus the company was now privately owned by Steinberg and his family. In 1986, however, the company again went public selling about 20% of its stock with Steinberg and his family retaining the rest.

The company's stock value plummeted following the stock market crash of 1987 and its underwriting results suffered, in large part due to claims arising from hurricanes and the 1989 San Francisco earthquake. All the while, however, Reliance's growth strategy continued, expanding into ever more diversified insurance markets, including surety and reinsurance. Beyond the expansion of its insurance markets, Reliance Group developed other areas of business; among which, Reliance Development Group, Inc. handled real estate operations, and Reliance Consulting Group provided consulting services for energy, environment, and natural resources. As the company expanded in one area through start-up and acquisition, it meanwhile sold off other interests. In 1989 the company's sale of Days Corporation, owner of the Days Inn hotel chain, nearly tripling its initial 1984 investment.

Although it was hushed at the time, Saul Steinberg suffered a stroke in 1995. Active control of his financial empire was assumed by his brother, Robert Steinberg. Changes were instituted ostensibly toward making Reliance more focused on insurance, and for a while, it looked as if the company was prospering. Many investors who had long ago grown weary of Saul Steinberg were endorsing the company. RGH stock reached a record high. The company reported in its 1998 annual financial statement, filed in March 1999, a $1.7 billion statutory surplus, its largest in history, and a profit for that year of $585 million. Within less than three years, however, the Commonwealth Court of Pennsylvania would issue a court order placing Reliance into liquidation. The company lost $177 million in net income in 1999 and another $198 million in 2000. In early 2000 Reliance agreed to be acquired by Leucadia National for stock that amounted to only $359 million. The price represented a market capitalization loss of $1.941 billion since mid-1998 when Reliance’s market value reached a high of $2.3 billion. The deal, however, fell through when Leucadia National backed out because of concerns over Reliance's financial health.

Pennsylvania insurance regulators sought to salvage the company in 2001, but by October 3 of that year, following the undermining of the financial markets in the wake of the terrorist attacks of September 11, 2001, Pennsylvania's insurance commissioner, Diane Koken, petitioned to have the company liquidated. It was the largest insurer liquidation in U.S. history according to the Insurance Information Institute.

The speed and size of Reliance's collapse in turn caused uncertainty about the foremost insurance rating agencies, such as A.M. Best Co., who until June 2000 rated Reliance's financial strength as an A- (excellent), and Standard & Poor's, who had assigned the insurer an A(strong) rating. The rating agencies, however, played an integral role in the company's collapse. Once A.M. Best downgraded Reliance's rating in June 2000, due in part to the substantial debt of the parent company, Reliance Group Holdings, Inc., Reliance ability retain and attract business was dealt a fateful blow. Another factor causing the sudden downfall was a complicated reinsurance pool of workers compensation policies, dubbed Unicover, that was a very costly failure. Unicover, however, was only one example of the corporate mentality and risk-taking philosophy that ultimately caused the company's demise. In its eagerness to expand and grow, policies were written too cheaply; excessive dividends were paid to stockholders (largely the Steinbergs themselves); and the company was mismanaged. And as a result it failed.

Related Collections

Additional Information

Certificates carry no value on any of today's financial indexes and no transfer of ownership is implied. All items offered are collectible in nature only. So, you can frame them, but you can't cash them in!

All of our pieces are original - we do not sell reproductions. If you ever find out that one of our pieces is not authentic, you may return it for a full refund of the purchase price and any associated shipping charges.